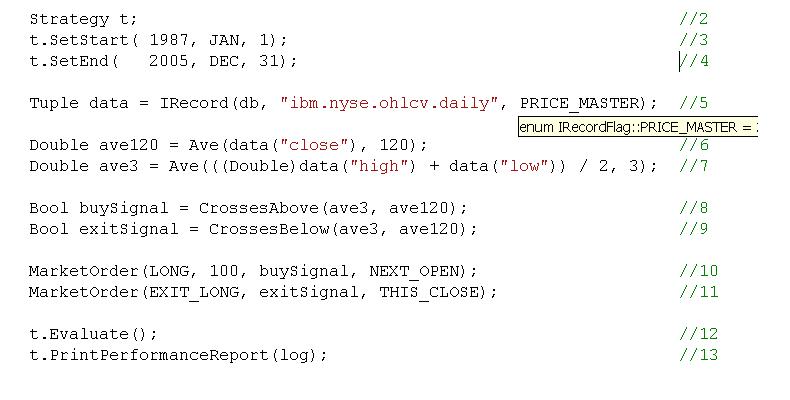

Time Series API Screenshot

Time Series API is a professional C++ class library for simulating (backtesting) and deploying financial trading strategies as well as general purpose time series modelling. The library is a stand-alone time series engine that can be extended via a component object model.

Models are defined using 'formula syntax and semantics' made possible by a set of lightweight interface classes that supersede the component framework. The library supports the modelling of even the most complex ideas, is easily extended, and supports deployment in any timeframe (variable or fixed, with intervals as short as one millisecond). The library also benefits from a set of highly optimized database classes for reading and writing millions of records in seconds.

As a general purpose tool for modelling time series, Time Series API has applications in many domains, such as:

* Trading and investment strategy simulation and deployment:

- Individual market and inter-market models

- Iterative evaluations on baskets

- Evaluation on aggregates (e.g. custom indices)

- Fundamental company data models

* Economic modelling

* Time series normalization and processing:

- Normalizing neural training data

- Data transformations

- Timeframe conversions

* Data monitoring (e.g. financial, scientific):

- Event Notification

- Pattern recognition

- Filtering applications, (e.g. noise reduction)

* Computational modelling

- Genetic algorithms

Back to Time Series API Details page

- Time Series Reports

- Zaitun Time Series

- Comparing Time Series

- Time Series Data

- Excel Comparing Time Series

- Flex Time Series Chart

- Commercial Series

- Series World

- Dad Tv Series

- Moonlight Tv Series